Real Estate Investment

Cap Rate Calculator: How to Calculate Cap Rate on South Florida Investment Properties

June 9, 2026 · 5 min read · By Pure Equity Realty

Cap rate is the foundational metric for evaluating South Florida investment properties. Here's exactly how to calculate it, what the numbers mean, and how to use reverse cap rate to find your maximum purchase price.

A reverse cap rate calculator is one of the most practical tools a South Florida investor can use. Cap rate (capitalization rate) lets you compare properties of different sizes and prices on a level basis, and flipping the formula to solve for price tells you exactly what to pay, rather than guessing. Here is how to calculate it and how to use the reverse cap rate to work backwards from your target return.

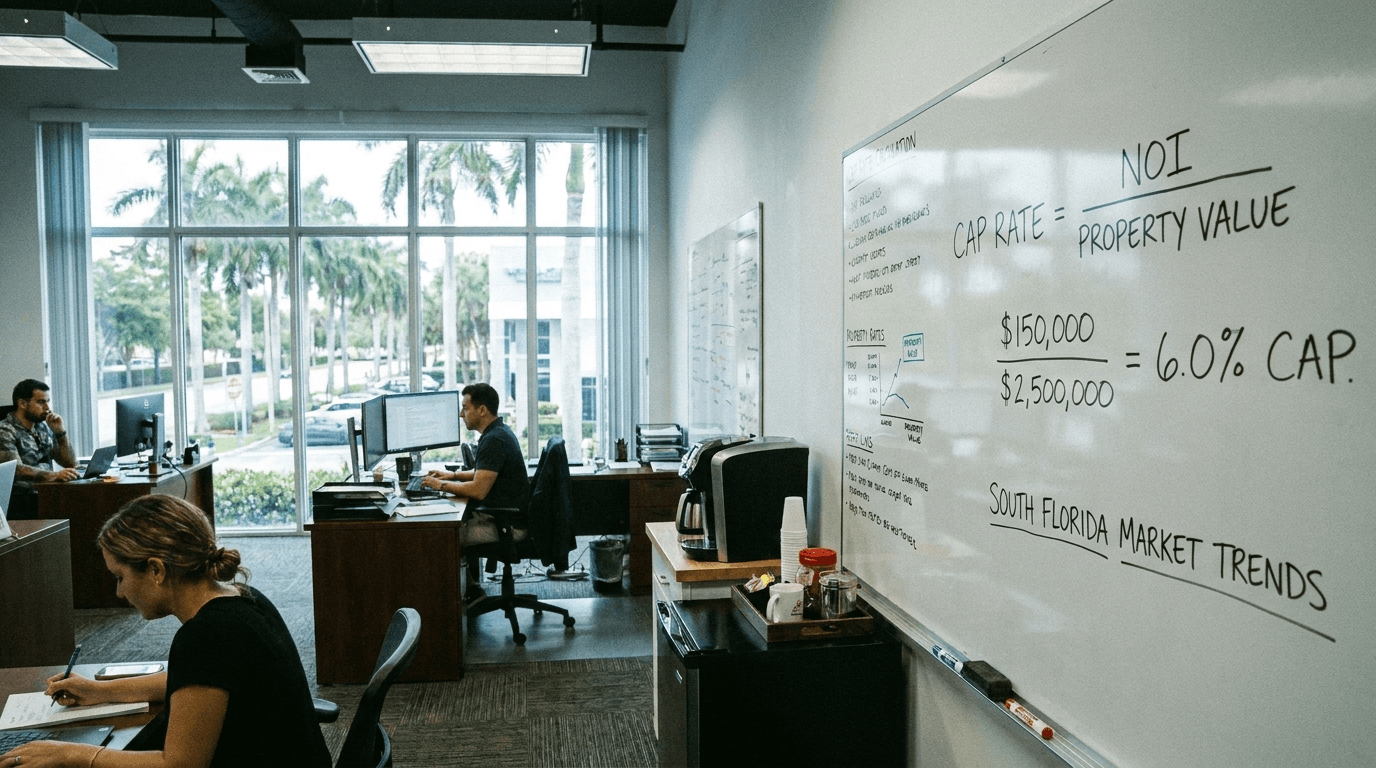

The cap rate formula

Cap Rate = Net Operating Income (NOI) divided by Property Value (or Purchase Price)

Where:

- Net Operating Income (NOI): Gross Annual Rent minus Vacancy Loss minus Operating Expenses (taxes, insurance, management, maintenance, repairs, but NOT mortgage payments)

- Property Value: Current market value or the price you are considering paying

Example: A South Florida single-family rental priced at $400,000 rents for $2,400/month ($28,800/year). After 7% vacancy ($2,016) and operating expenses of $9,500 (taxes, insurance, management, maintenance), NOI comes to $17,284. Cap Rate = $17,284 divided by $400,000 = 4.3%.

What good cap rates look like in South Florida by market

Cap rates vary significantly across South Florida's counties and by property type:

- Coastal Palm Beach and Broward (luxury/primary homes): 3 to 4.5%. These markets are appreciation-driven. Investors accept lower current income in exchange for strong long-term price growth.

- Inland Broward and West Palm Beach (workforce housing): 4.5 to 6%. Better cash flow with moderate appreciation.

- St. Lucie and Martin Counties: 5.5 to 7% or higher. Stronger cap rates, growing markets, lower entry prices.

- Highlands County: 6 to 8% or higher for stabilized residential. Less appreciation history, but strong income-to-price ratios.

- Small multifamily (2 to 4 units) across all markets: Generally 0.5 to 1% higher cap rates than single-family equivalents, due to economies of scale.

Reverse cap rate: working backwards from your target return

Reverse cap rate is how investors determine their maximum purchase price given a target return. The formula flips:

Maximum Price = NOI divided by Target Cap Rate

Example: You need a 6% cap rate to meet your return requirements on a Port St. Lucie rental. The property's NOI is $14,400/year. Maximum price = $14,400 divided by 0.06 = $240,000. If the seller is asking $280,000, the deal does not hit your required cap rate. You now have a clear, objective basis for negotiating or walking away.

Cap rate vs. cash-on-cash return: what is the difference?

Cap rate assumes no mortgage. It evaluates the property's income as if purchased with all cash, which makes it useful for comparing properties regardless of how they are financed. Cash-on-cash return accounts for your actual mortgage, measuring the return on your invested equity only. Both matter:

- Use cap rate to compare properties and assess market pricing.

- Use cash-on-cash (or our Rental Property ROI Calculator) to evaluate actual returns given your specific financing.

A property with a 5% cap rate can produce a 7 to 9% cash-on-cash return with the right leverage, because positive leverage amplifies the return on your invested equity. High leverage in a low-cap-rate market can produce negative cash-on-cash. Understanding both metrics gives you the full picture on any South Florida deal.

Run the numbers on a South Florida investment property

Our calculators let you model NOI, cap rate, and reverse cap rate in seconds. Start with the Cap Rate Calculator, then stress-test financing with the Rental Property ROI Calculator.

Ready to tour properties that hit your return targets? Talk to a Pure Equity agent.

Frequently asked questions

What is a good cap rate for South Florida?

It depends on the market and your goals. Coastal markets in Palm Beach and Broward typically run 3 to 4.5% because appreciation is the primary return driver. Inland workforce housing trades at 4.5 to 6%, and markets like St. Lucie, Martin, and Highlands counties can reach 6 to 8% on stabilized assets. There is no single "good" number. The right cap rate is the one that meets your required return given your risk tolerance and hold period.

Does cap rate include mortgage payments?

No. Cap rate is a pre-financing metric. It uses NOI, which excludes debt service. This is intentional because it lets you compare properties regardless of how they are financed. To model returns with a specific mortgage, use cash-on-cash return or a full ROI analysis.

What expenses go into NOI?

Property taxes, insurance, property management fees, routine maintenance, repairs, and any other recurring operating costs. Exclude mortgage principal and interest, depreciation, and capital expenditures (large one-time repairs). Some investors also exclude capital reserves, though including a reserve line produces a more conservative and realistic NOI.

How do I use the reverse cap rate to negotiate?

Calculate the NOI the property actually generates (not the seller's pro forma), then divide by your target cap rate. That result is your maximum price. If the asking price is above it, you know exactly how far apart you are and can present the math to support a lower offer. If the gap is too large, the deal does not work at that price, and you move on.

Can I use cap rate for single-family rentals?

Yes, though cap rate is more commonly used for commercial and multifamily properties. Single-family rentals often trade on GRM (gross rent multiplier) in addition to cap rate, partly because operating expenses can vary more per unit. That said, cap rate analysis on a single-family rental is still valid and useful, especially when comparing it against multifamily alternatives in the same market.