Real Estate Investment

Cash Flow Rental Property Calculator: How to Use It and What to Look For

June 9, 2026 · 6 min read · By Pure Equity Realty

A cash flow rental property calculator is the most important tool in a rental investor's arsenal. Here's how to use one correctly, what inputs matter most, and what the South Florida numbers actually look like.

A cash flow rental property calculator is the first thing you should run on any investment property before you make an offer. It tells you whether a property will put money in your pocket every month or quietly drain it. In South Florida's market, where insurance costs and HOA fees can dramatically affect returns, using a reliable calculator with accurate inputs is not optional.

What a cash flow rental property calculator actually measures

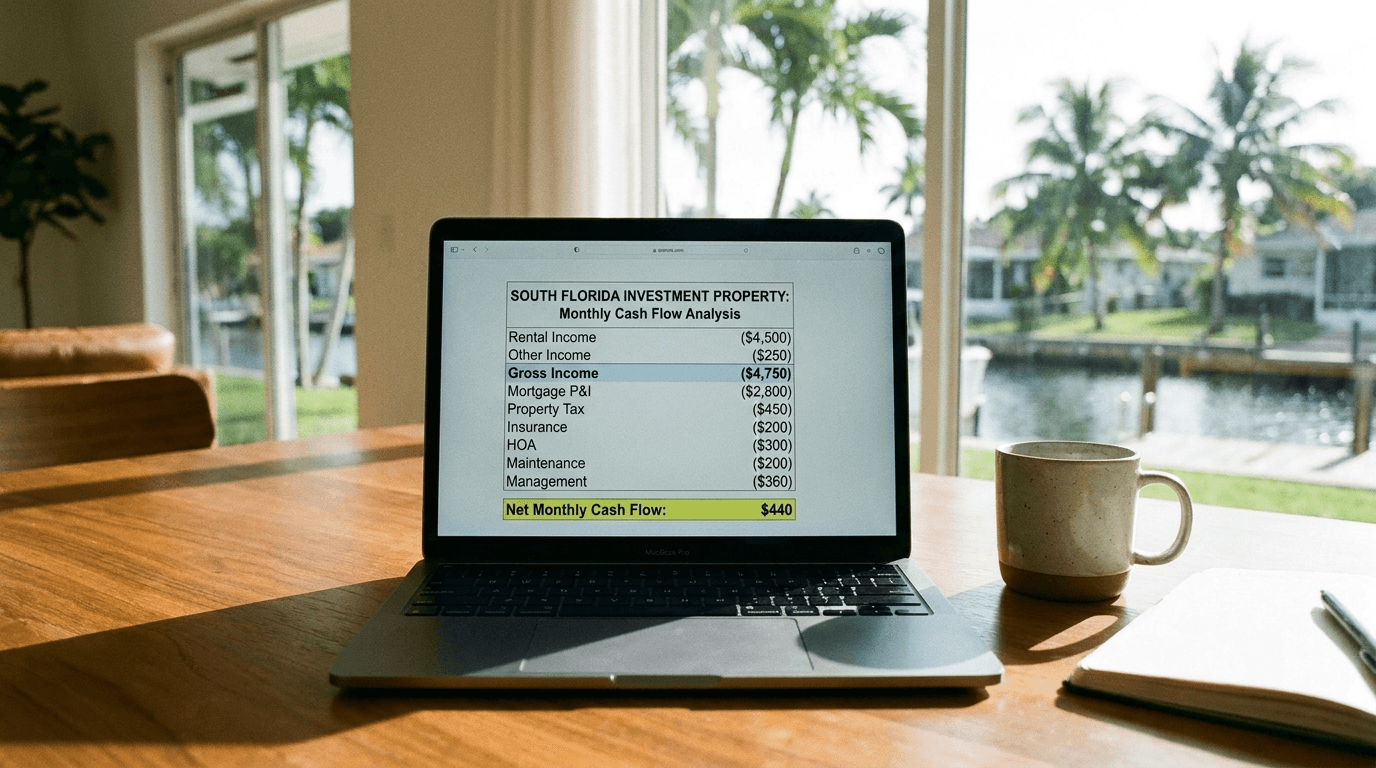

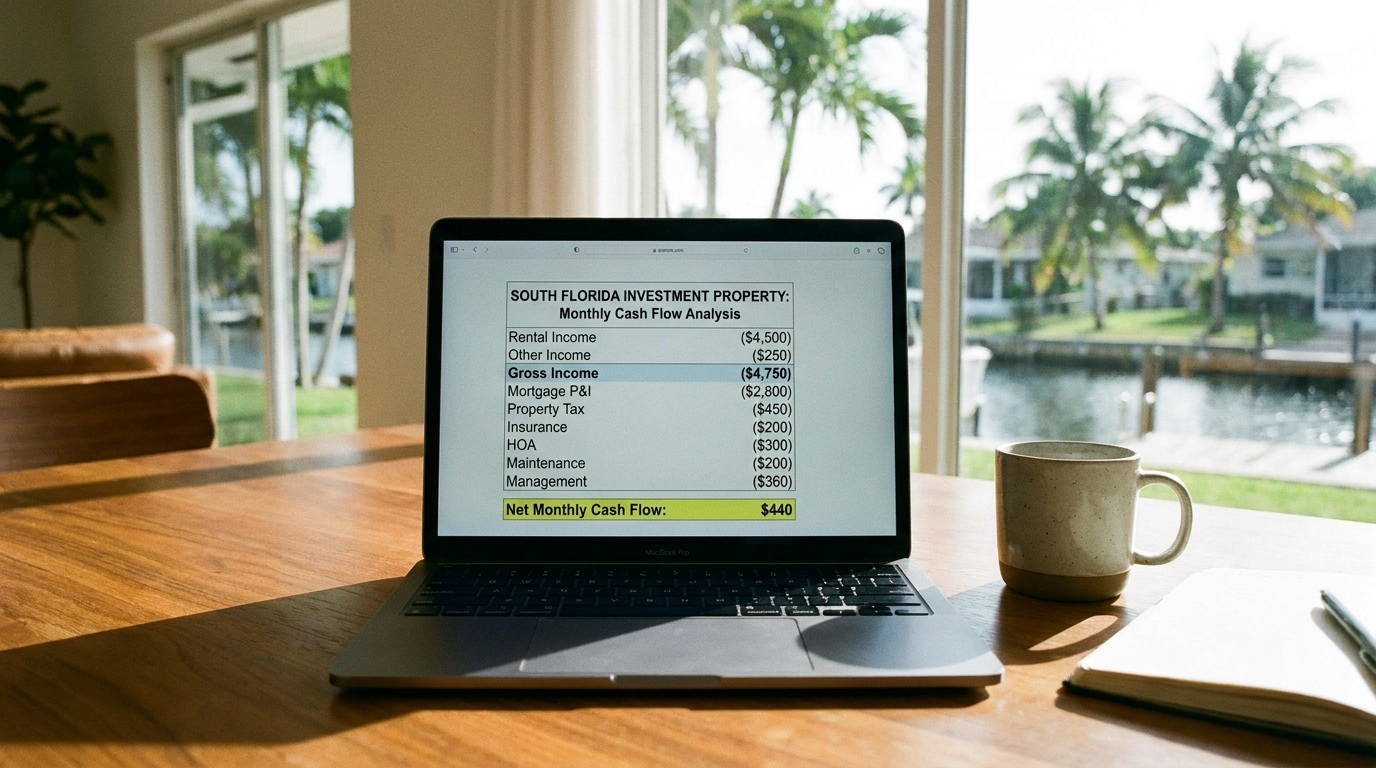

Net cash flow is the money remaining after all expenses are paid, including the mortgage. It is the truest measure of a rental property's performance because it accounts for your actual financing structure, not just the property's theoretical value. Two investors buying the same property at the same price can have dramatically different cash flows based on their down payment and loan terms.

The basic formula:

- Gross rental income

- Minus vacancy (typically 5-8% in South Florida)

- Minus operating expenses (taxes, insurance, maintenance, management, HOA)

- Minus debt service (mortgage principal + interest)

- Equals net cash flow

The inputs that most investors get wrong

Running a cash flow calculator with bad inputs gives you a false sense of security. These are the numbers South Florida investors most commonly underestimate:

- Insurance. Florida homeowner's insurance, especially in coastal Palm Beach, Broward, and Miami-Dade counties, has increased 30-60% in recent years. Get an actual insurance quote before you close. Do not use the current owner's premium as your estimate.

- Property taxes. When a South Florida property sells, it gets reassessed at the new purchase price. The previous owner's tax bill (often protected by homestead exemption) can be dramatically lower than what you will pay. Check the county property appraiser's website for estimated post-sale taxes.

- Maintenance reserve. Budget 8-10% of annual gross rent for repairs and maintenance. South Florida's climate is hard on HVAC systems, roofing, and exterior paint. Investors who budget 5% routinely come up short.

- Vacancy. Use 7-8% as a baseline. Even in tight rental markets, turnover and lease-up periods mean you will not collect 100% of rent every year.

What good cash flow looks like in South Florida

In South Florida's current market, here is what realistic cash flow looks like by strategy:

- Leveraged single-family (25% down, 7% rate): $150-$500 per month net in most Palm Beach and Broward markets. Tighter than most calculators suggest when insurance is input correctly.

- All-cash single-family: $900-$1,400 per month net. No mortgage payment, but much more capital deployed per property.

- Small multifamily (2-4 units), leveraged: $400-$900 per month total net. The combined rents from multiple units create more cushion.

- Short-term rental (coastal areas): $1,500-$4,000 per month net potential, but management costs are higher and regulatory risk is real.

Use our free South Florida rental calculator

Our Rental Property ROI Calculator was built for South Florida investors. It calculates monthly cash flow, annual cash-on-cash return, cap rate, and total 5-year return, all with South Florida-realistic default assumptions you can customize to your specific deal.

Run every property you are considering through the calculator before you make an offer. If the numbers do not work with realistic inputs, walk away regardless of how good the property looks in person. Our team can help you interpret the results and find deals that actually pencil out. Reach out here or explore investment opportunities by county. For more on rental property analysis, see IRS rental income guidelines for tax context.