Home Buying Tips

Earnest Money in Real Estate: How It Works in South Florida

June 9, 2026 · 6 min read · By Pure Equity Realty

Earnest money is your good-faith deposit, it shows sellers you're serious, but it comes with real risk if you walk away at the wrong time. Here's how it works in South Florida.

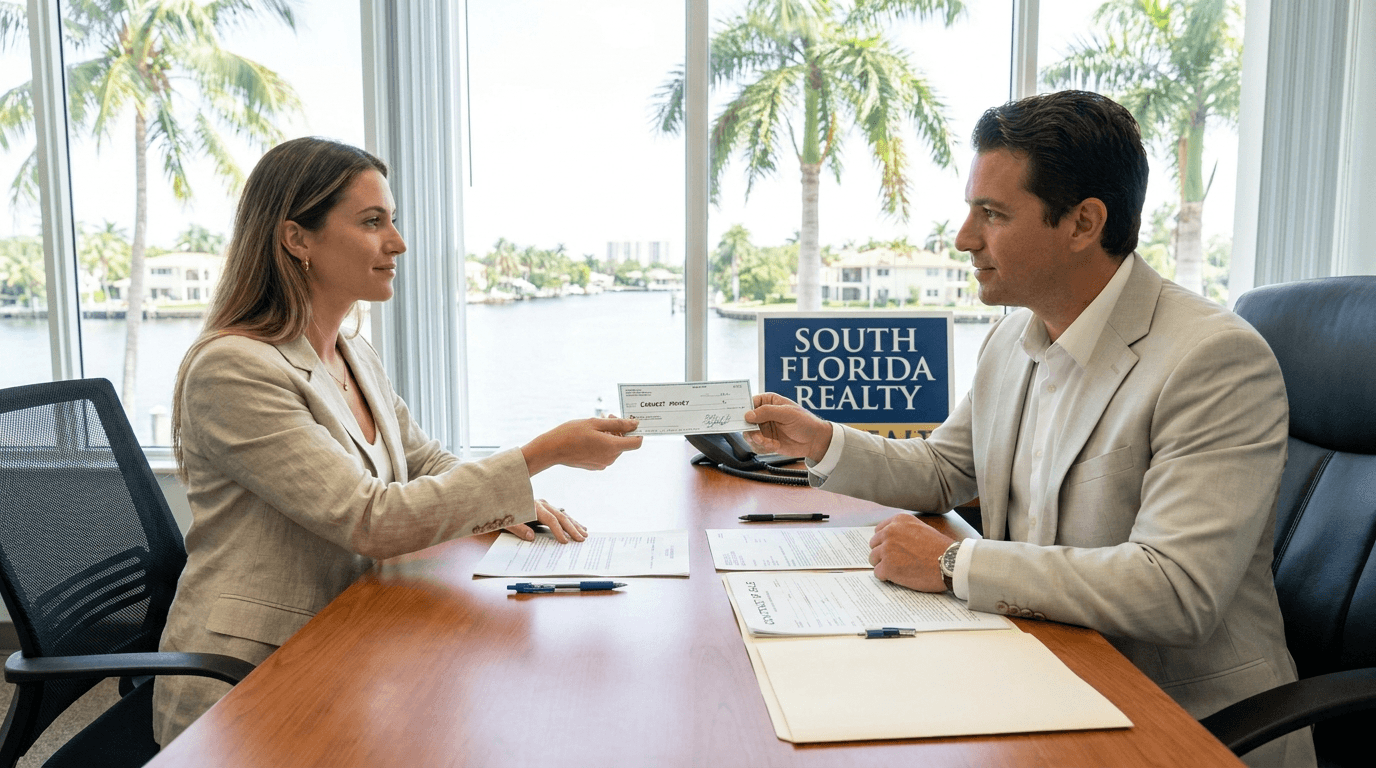

When you make an offer on a home in South Florida, you'll typically be asked to put down an earnest money deposit, a sum paid upfront to show that you're a serious buyer. It's held in escrow by a title company or real estate broker and applied toward your down payment or closing costs at closing. If the deal falls apart under the wrong circumstances, though, you could lose it entirely. Knowing how earnest money real estate rules work in Florida is essential before you sign anything.

How much earnest money is standard in South Florida?

In South Florida, earnest money deposits typically run from 1% to 3% of the purchase price. On a $500,000 home, that works out to $5,000 to $15,000. On luxury properties or in a competitive multiple-offer situation, sellers sometimes expect more, in the 3% to 5% range, because a larger deposit signals real financial commitment. Cash buyers often face that higher expectation too, since they typically waive contingencies that would otherwise give them an exit.

The amount is negotiable and spelled out in the contract. A larger deposit reassures the seller; a smaller one limits your exposure if something goes sideways.

Who holds earnest money?

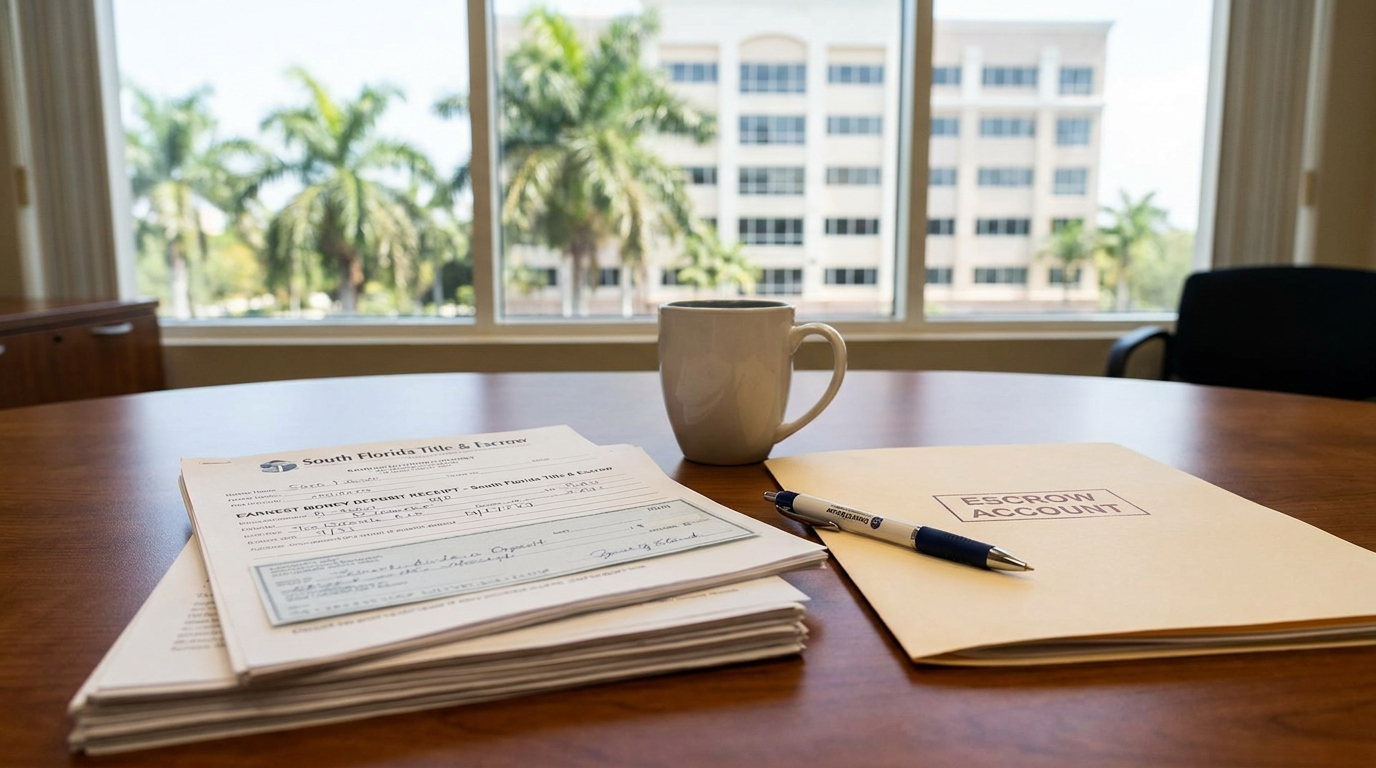

In Florida, earnest money is typically held by the title company or the listing brokerage's escrow account. State law requires these funds to sit in a separate escrow account, kept apart from operating funds entirely. The escrow agent holds the money in a neutral position until the transaction closes or a dispute resolution process directs how it gets distributed.

When can you get your earnest money back?

Florida's standard FAR-BAR (Florida Association of Realtors / Florida Bar) residential contract includes several contingencies that protect your deposit:

- Financing contingency: if you can't obtain a mortgage at the agreed terms, you can typically cancel and recover your earnest money.

- Inspection contingency: during the inspection period (often 10 to 15 days), you can walk away for any reason and get your deposit back in full.

- Appraisal contingency: if the property appraises below the contract price and the parties can't agree on a new number, the buyer can exit with the deposit.

- Title defect contingency: if a clear title cannot be delivered, the buyer can cancel and recover the deposit.

- HOA review period: Florida law gives buyers a window to review HOA documents; canceling within that period also protects the deposit.

When can you lose your earnest money?

You risk losing your deposit if you back out of the contract outside a contingency window or without a valid contractual reason. Common situations where buyers forfeit their money include:

- Walking away after the inspection period expires without a documented defect

- Failing to secure financing when no financing contingency was included in the contract

- Changing your mind after all contingencies have been waived or removed

- Missing a required deposit deadline or document submission date written into the contract

Under Florida law, when a buyer defaults the seller's remedy is ordinarily limited to keeping the earnest money deposit (liquidated damages), unless the contract says otherwise. That cap is actually a meaningful protection for buyers. Your worst-case financial exposure is the deposit itself, not the seller's carrying costs or lost profit.

Earnest money vs. down payment

Earnest money is not an extra cost on top of your down payment. It's a credit applied toward what you owe at the settlement table. Put $10,000 in earnest money on a $500,000 home with a 20% down payment, and you'll bring $90,000 to closing instead of $100,000. The deposit counts.

One thing buyers sometimes miss: the timing. Most South Florida contracts require the earnest money deposit to be wired within one to three business days of the effective date. Miss that window and the seller may have grounds to cancel the contract.

Practical tips for South Florida buyers

Here's what tends to matter in this market specifically:

- Wire funds from an account that can clear quickly. Personal checks cause delays and some sellers won't accept them.

- Keep a copy of your escrow wire confirmation. You'll need it if there's ever a dispute.

- If you're making an offer in a multiple-bid situation, your agent may suggest increasing the deposit to stand out. That's legitimate, but make sure the inspection period is long enough for you to vet the property before that window closes.

- Read the default and dispute clause in the contract before you sign, not after. The FAR-BAR contract has a specific process for releasing disputed funds, and it takes time.

Ready to make an offer in South Florida?

Our agents know Palm Beach, Broward, and Miami-Dade inside out. We'll walk you through offer strategy, earnest money amounts, and every contingency before you sign. Contact us to get started, or explore our homes for sale to see what's on the market now.

Frequently asked questions

Is earnest money required by Florida law?

No. Florida law does not require an earnest money deposit for a real estate contract to be valid. In practice, though, sellers expect one. A contract with no deposit raises questions about whether the buyer is truly committed, and most sellers won't accept those terms in a normal market.

What happens to earnest money if the seller backs out?

If the seller defaults, the buyer is entitled to a refund of the full deposit. The buyer may also have the right to pursue specific performance (forcing the sale to proceed) or sue for damages, depending on the contract language and circumstances.

How long does it take to get earnest money back after a canceled deal?

If both parties agree in writing to release the funds, the escrow agent can distribute the money within a few business days. If there's a dispute, Florida requires the escrow holder to follow a specific procedure that can take 30 days or more, including sending written notices and potentially going to mediation or a court interpleader action.

Can earnest money be negotiated after the offer is accepted?

Generally, no. Once both parties have signed the contract, the deposit amount and terms are binding. Any change would require a written addendum signed by both the buyer and seller.

What is a "hard" earnest money deposit?

A hard deposit (sometimes called "going hard") means the buyer has agreed to make the earnest money non-refundable after a certain date or milestone, such as the end of the inspection period. This is common in new construction contracts and occasionally in competitive resale situations. If you're asked to go hard, make sure you've completed all due diligence before that date arrives.