Real Estate Investment

How to Calculate Cap Rate in South Florida Real Estate

June 9, 2026 · 7 min read · By Pure Equity Realty

Cap rate is the most important metric for evaluating investment property, and one of the most misunderstood. Here's exactly how to calculate it and what the numbers mean in South Florida's market.

If you're evaluating an investment property in South Florida, the cap rate (capitalization rate) is the first number experienced investors reach for. It gives you a quick, financing-agnostic snapshot of a property's income potential relative to its price. Like most useful metrics, though, it's frequently misunderstood, misapplied, or cherry-picked by sellers trying to make a deal look better than it is. Here's how to calculate cap rate correctly and what the numbers actually mean in Palm Beach, Broward, Miami-Dade, and beyond.

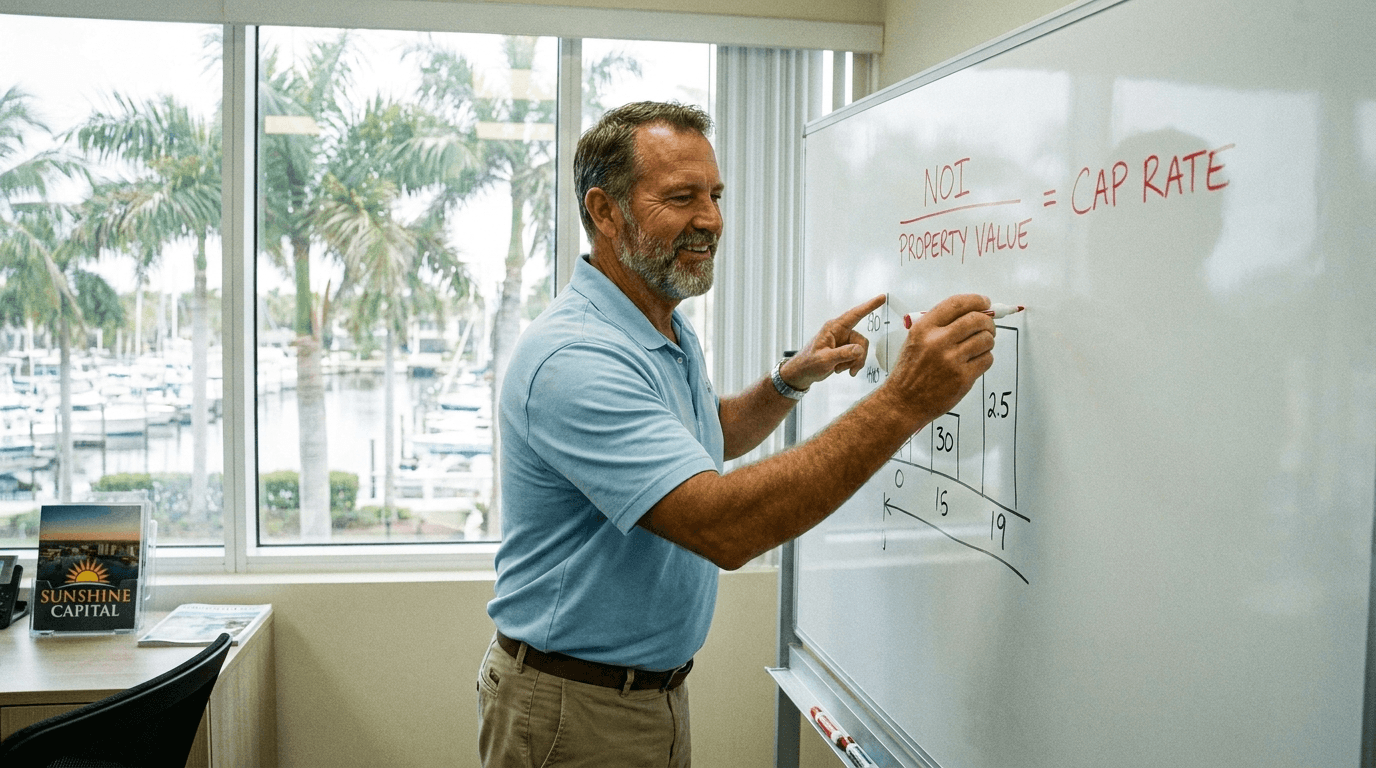

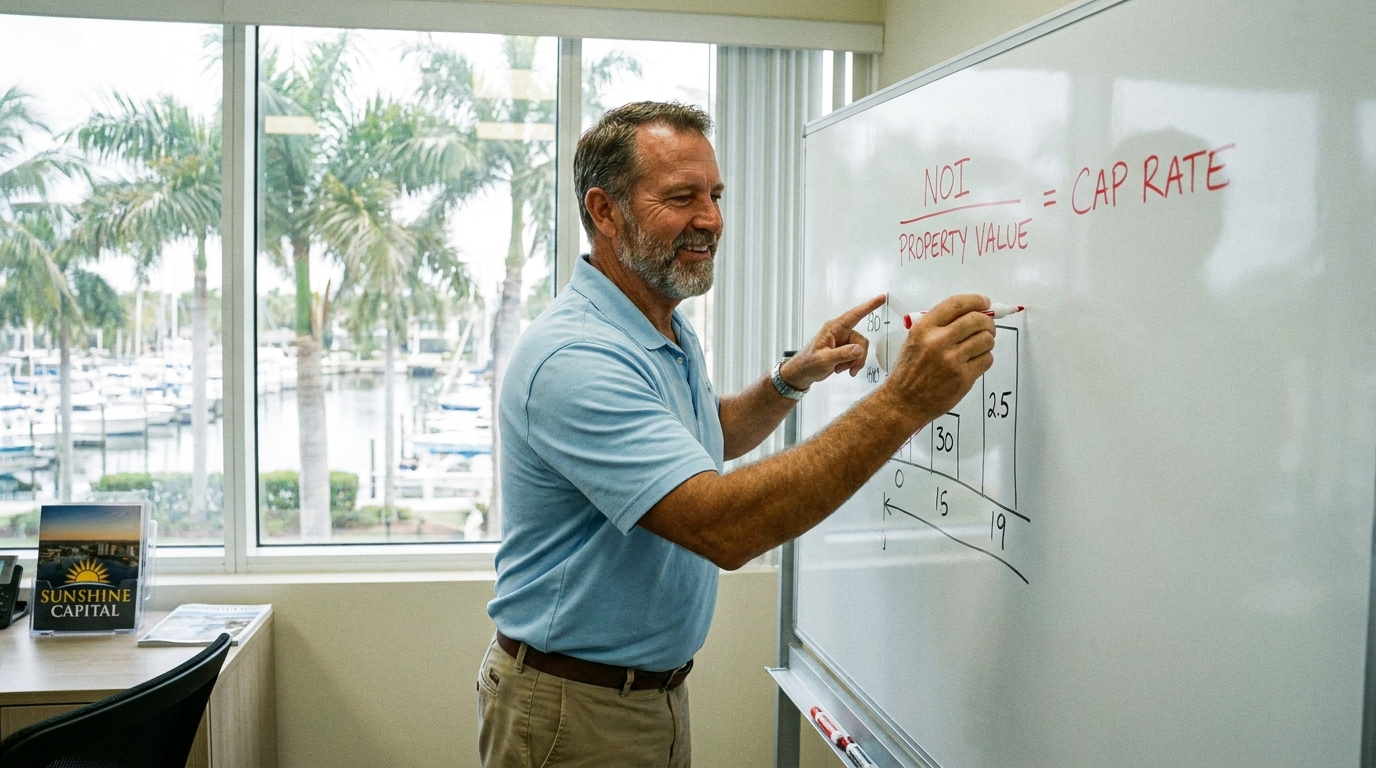

The cap rate formula

The formula is simple:

Cap Rate = Net Operating Income (NOI) / Current Market Value (or Purchase Price)

Net Operating Income is the annual income a property generates after all operating expenses, but before mortgage payments and income taxes. The key word is "operating": NOI excludes debt service intentionally, so you can compare properties regardless of how they're financed.

Example: A duplex in Delray Beach generates $36,000/year in gross rents. After vacancy (5%), property taxes, insurance, property management (10%), maintenance reserves, and HOA fees, you're left with $22,000 in NOI. If the property costs $440,000, the cap rate is $22,000 / $440,000 = 5.0%.

What goes into NOI: common mistakes

The most common mistake investors make is using gross rental income as a proxy for NOI. Sellers and their agents will sometimes advertise "5% cap rate" using an NOI that only deducted taxes and insurance, ignoring vacancy, management fees, capital reserves, and maintenance. Always build your own NOI from scratch using realistic assumptions:

- Gross potential rent: based on current market rents, not a seller's pro-forma

- Vacancy allowance: 5-8% is typical in South Florida's strong rental market

- Property management: 8-12% of gross rents if professional management is used

- Property taxes: verify the actual tax bill; South Florida taxes can be high, especially after homestead exemption loss

- Insurance: get your own quote; South Florida insurance costs have risen sharply in recent years

- HOA fees: if applicable, these reduce NOI directly

- Maintenance and capital reserves: 5-10% of gross rents is a reasonable placeholder

Cap rates by area in South Florida (2026)

Cap rates vary meaningfully across South Florida's counties. As a general guide in 2026:

- Miami Beach / Brickell / Coconut Grove: 3-4%. Ultra-low cap rates driven by appreciation speculation and international demand.

- Fort Lauderdale / Boca Raton / Palm Beach Gardens: 4-5.5%. Strong markets with some income potential.

- Inland Broward / Palm Beach (Lauderhill, Lake Worth, Boynton Beach): 5-6.5%. Better cash flow territory.

- St. Lucie and Martin Counties: 5.5-7%. Emerging markets with better yields.

- Highlands County: 7-9%+. Highest yields, with lower appreciation expectations.

Cap rate vs. cash-on-cash return

Cap rate ignores your financing. It measures the property, not your investment structure. Cash-on-cash return (annual pre-tax cash flow divided by total cash invested) tells you what your actual dollars are earning after debt service. Both metrics matter. Cap rate tells you whether the property is priced well; cash-on-cash tells you whether your deal works given your specific financing.

Use our Rental ROI Calculator to model both cap rate and cash-on-cash return on any South Florida property you're evaluating. Or contact our team for a full investment analysis on specific properties in your target market.