Market Updates

Interest Rates vs. House Prices in South Florida: What the Data Actually Shows

June 9, 2026 · 6 min read · By Pure Equity Realty

Conventional wisdom says higher interest rates crash home prices. South Florida's market keeps proving that wrong. Here's what the data actually shows about the interest rates vs house prices relationship, and why this market behaves differently.

The conventional wisdom about interest rates vs. house prices is simple: rates go up, prices go down. It makes intuitive sense. Higher rates reduce buying power, so buyers can afford less, so prices fall. But South Florida's real estate market has consistently defied this logic. Understanding why is essential for buyers, sellers, and investors making decisions here. Looking at any interest rates vs house prices graph, you will notice the relationship is rarely as clean as the theory suggests.

What the national data shows

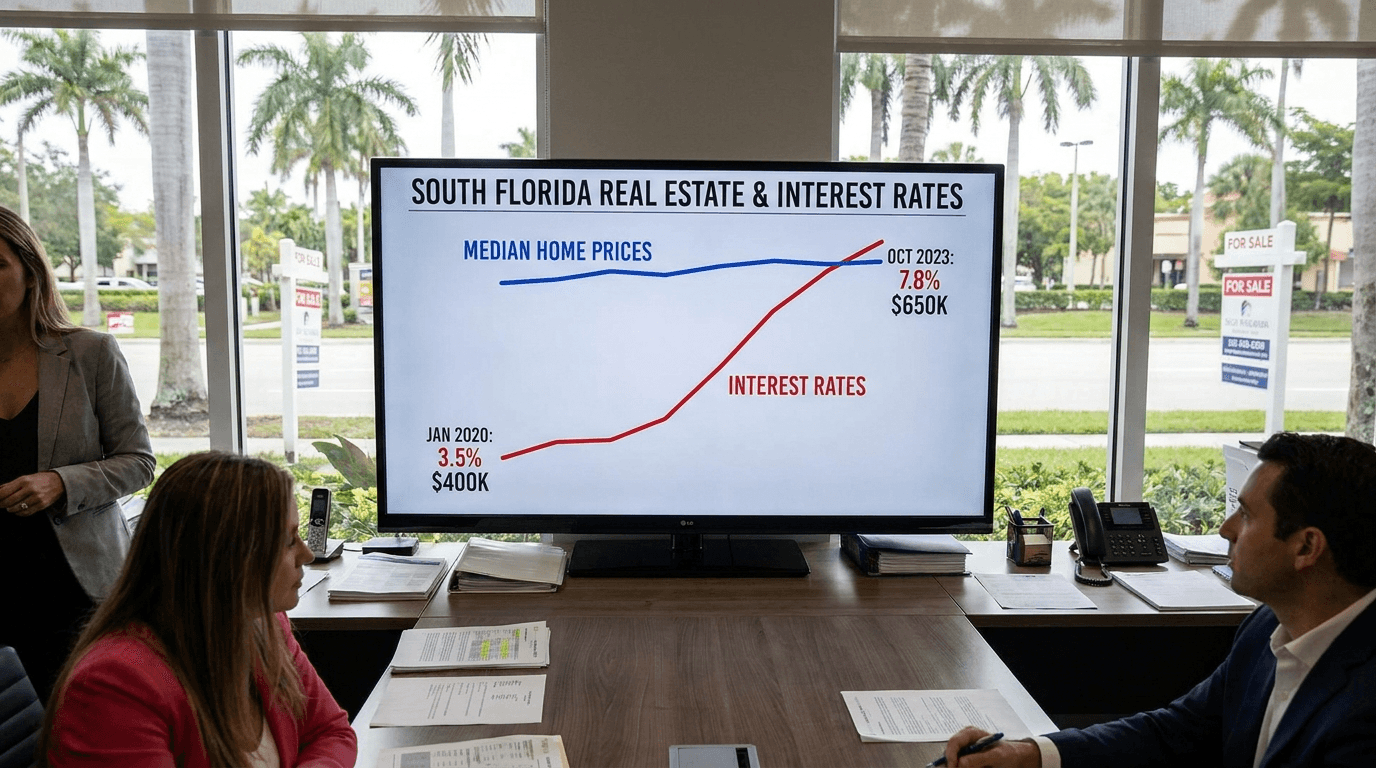

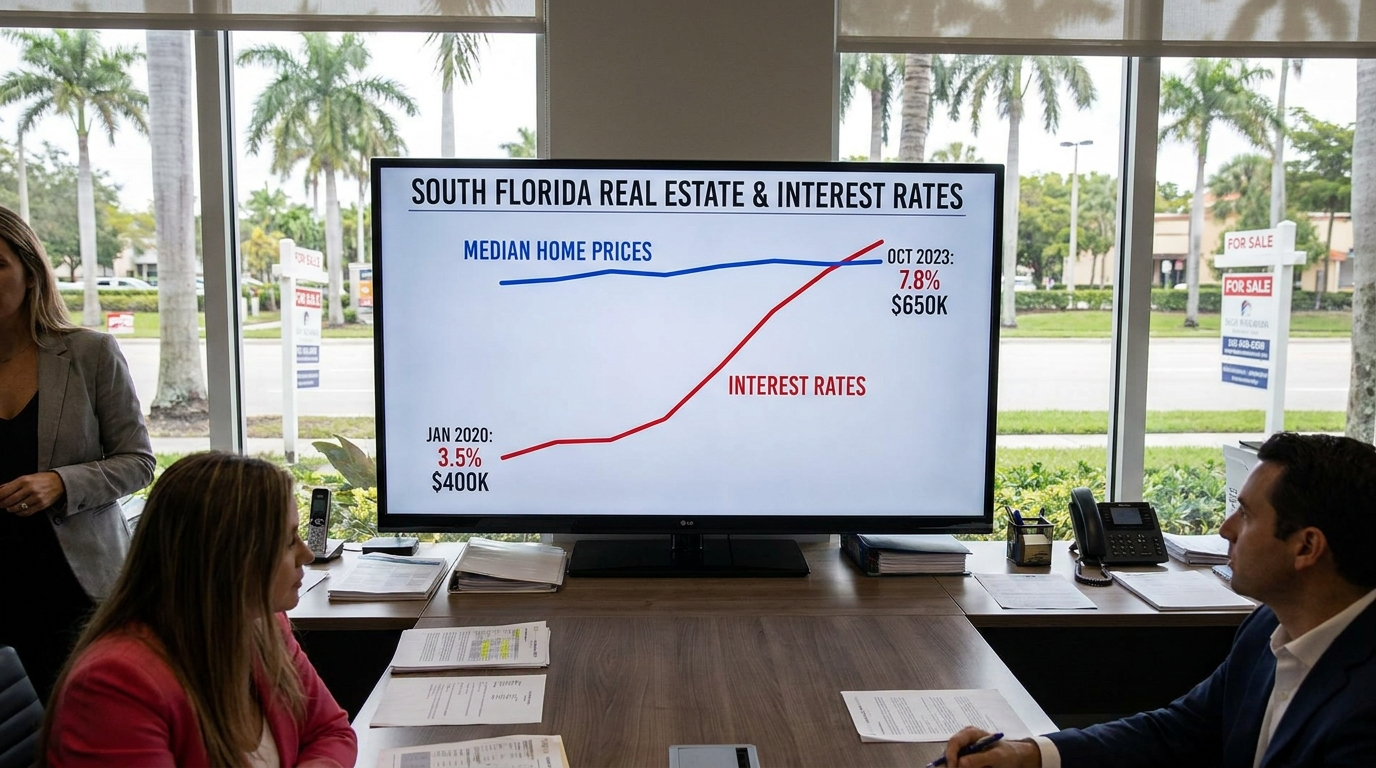

Nationally, there is a historical inverse relationship between interest rates and home prices, but it is weaker and slower than most people assume. When the Fed raised rates aggressively in 2022-2023, national median home prices dipped modestly in some markets and then resumed climbing. The reason: housing supply did not increase commensurately with demand destruction. With fewer homes for sale, prices held even as buyers retreated.

The classic interest rates vs. house prices graph shows rates and prices moving in opposite directions over decades. The timing lag is often 18-36 months, and local supply conditions frequently overwhelm the rate effect entirely.

Why South Florida is different

South Florida's housing market has structural demand drivers that most of the country lacks. These factors insulate prices from interest rate pressure in ways that markets dependent on first-time buyers or rate-sensitive local employment do not experience:

- Cash buyers. In Palm Beach, Miami-Dade, and coastal Broward, cash transactions routinely represent 30-45% of all closings. Cash buyers are entirely unaffected by mortgage rate changes. When rates rise, they become relatively more competitive because they often face fewer financed buyers.

- International demand. South Florida attracts consistent buyer interest from Latin America, Europe, and Canada. Many purchase in cash or finance through foreign institutions at different rate structures. This demand is driven by political stability and lifestyle considerations, not the 10-year Treasury yield.

- Domestic migration. The ongoing influx of buyers from New York, New Jersey, California, and Illinois continues to sustain demand. Many arrive with equity from high-priced home sales. A buyer from Manhattan with $800,000 in equity from a co-op sale is not rate-sensitive in the same way a first-time buyer in Ohio is.

- Constrained supply. The Atlantic Ocean, the Everglades, and decades of existing development have left little new land to build on along the coast. Supply cannot expand quickly enough to absorb demand shocks, which keeps a floor under prices.

What happened to South Florida prices when rates rose in 2022-2024

When the Federal Reserve raised rates from near-zero to over 5% between 2022 and 2024, South Florida saw these results:

- Transaction volume fell 20-35% as rate-sensitive buyers stepped back

- Days on market increased modestly, from an average of 18 to 35-45 days in most submarkets

- Price reductions became more common, but median prices held or continued rising in most counties

- The luxury segment ($2M+) was largely unaffected because cash buyers dominated

Palm Beach County median prices continued rising through the rate hike cycle. Miami-Dade saw a brief plateau before resuming appreciation. Only the most rate-sensitive segments, such as entry-level condos and inland starter homes with thin margins, experienced meaningful price softening.

What this means for buyers and sellers in 2026

For buyers: don't wait for rates to fall before you buy, assuming prices will drop while you wait. South Florida's market structure makes that a losing strategy in most submarkets. Buy when the deal makes sense for your finances and refinance when rates improve.

For sellers: rate sensitivity does affect your buyer pool, particularly for properties priced below $600,000 where most buyers are financing. Price correctly from day one, and expect slightly longer days on market than during the zero-rate era.

For investors: rate increases compress leveraged returns. Model your deals at current rates, not the rates of two years ago. Our Rental Property ROI Calculator and Fix & Flip Calculator let you run scenarios at any rate. Check the Florida Realtors market statistics for current county-level data.