Home Buying Tips

Risks of Buying a Short Sale Home in South Florida

June 9, 2026 · 7 min read · By Pure Equity Realty

Short sales can deliver genuine below-market deals in South Florida, but they come with timeline uncertainty, condition risks, and approval complications that every buyer should understand before making an offer.

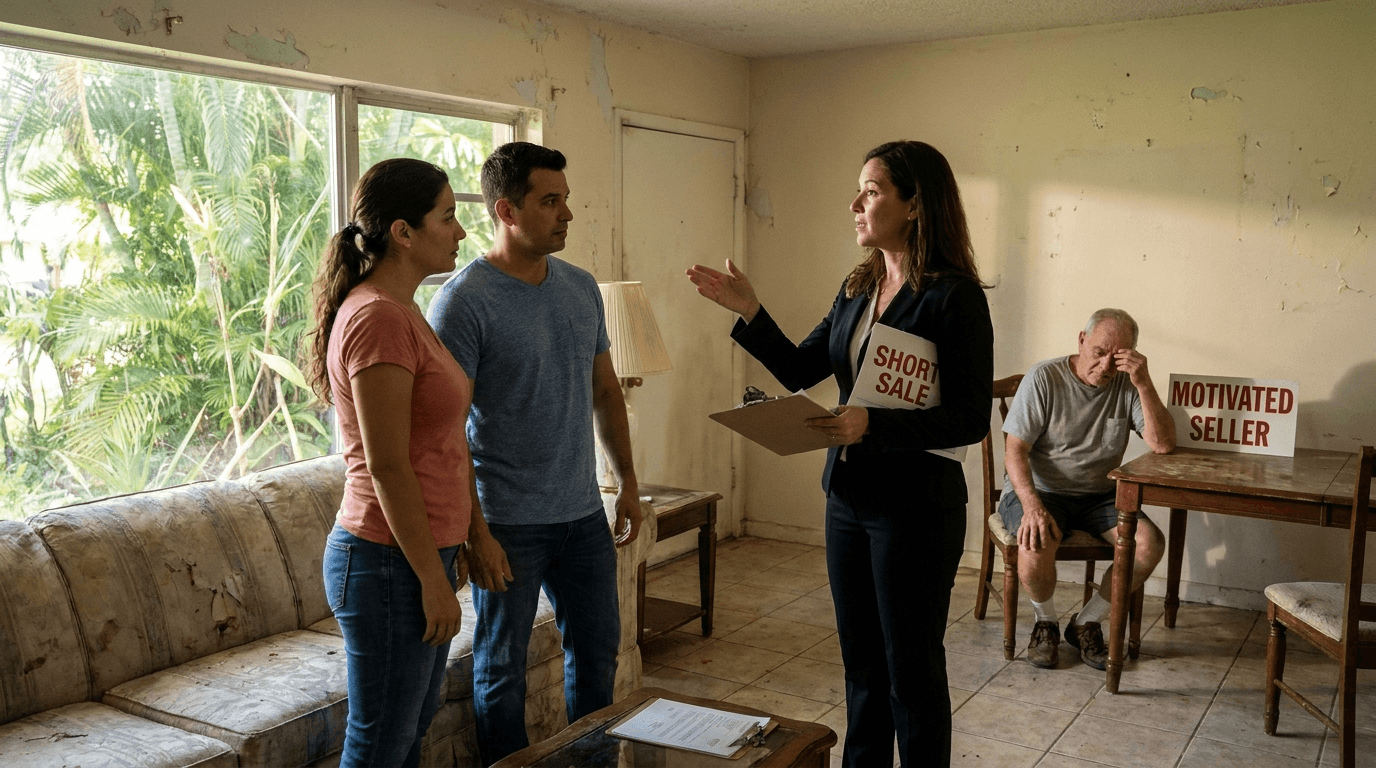

A short sale happens when a homeowner sells their property for less than the outstanding mortgage balance, with the lender's permission. On paper, this produces below-market deals for buyers. In practice, the risks of buying a short sale are real enough that many buyers and agents avoid them entirely. In South Florida's market, where distressed properties keep surfacing across Broward, Palm Beach, and Miami-Dade counties, knowing these risks is what separates buyers who close successfully from those who waste months and walk away empty-handed.

Risk #1: extended and uncertain timelines

Time is the biggest risk in any short sale. A standard South Florida transaction closes in 30 to 45 days. A short sale can take three to six months from accepted offer to closing, and some drag on longer. The lender has to review and approve the sale price, which means their own internal valuation (usually a BPO or full appraisal), a loss mitigation review, and investor approval if the loan has been securitized.

You can have a signed contract and be fully ready to close, then sit for months waiting on the bank. Your rate lock can expire. Your job situation can change. You can miss other properties you might have bought. Go in knowing that the timeline is not yours to control.

Risk #2: as-is condition

Short sale sellers are in financial distress. They have not been keeping up with maintenance, and they have no money for repairs. Lenders will not require or fund repairs as a condition of approval, so these properties almost always sell as-is.

In South Florida's climate, deferred maintenance compounds fast. A roof leak that has gone unaddressed for a year produces mold. HVAC systems in vacant homes fail. Pool equipment deteriorates. Budget conservatively for post-closing repairs and factor those costs into your offer price from the start, not after you fall in love with the property.

Risk #3: the bank may reject your offer

The seller signing your contract is just the first step. The lender still has to approve the sale price and terms. If the bank's BPO or internal valuation comes in above your contract price, they may counter at a higher number or reject the short sale outright. This happens more often than buyers expect, and it can happen after months of waiting.

If the lender counters at a price that no longer makes financial sense, you can walk away and recover your earnest money (assuming the contract is written correctly). You will not, however, recover the time you spent waiting.

Risk #4: title issues

Short sale properties often carry complex title situations. Beyond the primary mortgage, there can be second liens, HOA liens, tax certificates, judgments, or code enforcement violations that must be resolved before closing. The lender approving the short sale does not automatically clear other liens. Each one requires its own negotiation.

Use a title company with real short sale experience and order a full title search as early in the process as possible. Problems that surface months before closing can often be worked out. Problems that surface at the closing table often cannot.

Risk #5: deficiency judgment concerns affecting the deal

After a short sale closes, the lender may have the right to pursue the seller for the deficiency balance, which is the gap between the sale price and the full amount owed. Florida law provides important protections here, but sellers' concerns about deficiency judgments can cause them to stall or back out when approval is close.

As a buyer, you cannot control this. It is worth understanding, though, because a seller who turns uncooperative late in the process may be reacting to news about their own deficiency situation rather than anything you have done.

Should you buy a short sale?

The risks of buying a short sale are genuine, but so is the upside for the right buyer. If you have no hard deadline, a short sale in South Florida can deliver real below-market value. Work with an agent who has handled short sales before (not just one who has taken a course on them), structure the contract with proper protections, and budget honestly for both the purchase price and the work the property will need after closing.

Our team at Pure Equity Realty has worked through dozens of short sales across Palm Beach, Broward, and Miami-Dade counties. Contact us if you are weighing a short sale purchase, or learn more about the BPO process lenders use to evaluate short sale offers.

Thinking about buying distressed property in South Florida? Pure Equity Realty works with buyers across Palm Beach, Broward, and Miami-Dade counties. We know the short sale and foreclosure landscape here. Reach out to talk through your options, or browse current listings to see what is on the market now.

Frequently asked questions

How long does a short sale take in Florida?

Most short sales in Florida take three to six months from accepted offer to closing, though some take longer depending on the lender, the number of liens involved, and whether the loan has been securitized. Buyers should plan for at least 90 days and build that into any timeline-dependent decisions.

Can you negotiate the price on a short sale?

Yes, but you are negotiating with the lender, not the seller. The seller has limited leverage because the lender controls approval. The lender will order their own valuation, and if it comes in above your offer, they will counter or decline. A well-priced offer that reflects both market value and the property's condition gives you the best chance of moving forward without a protracted back-and-forth.

Is a short sale better than a foreclosure for a buyer?

Generally, yes. Short sales tend to be in better condition than bank-owned (REO) properties because the original owner is still in the home and has some motivation to maintain it. Title is usually cleaner because the sale is structured before the lender takes possession. The tradeoff is timeline: short sales take longer to close than most REO transactions.

Do short sales show up on your title search?

The short sale itself does not create a title issue, but the financial circumstances that lead to a short sale often do. Liens, judgments, unpaid HOA dues, and tax certificates can all attach to the property. A full title search early in the process is not optional on a short sale purchase.

Should I use a buyer's agent for a short sale?

Yes. A buyer's agent who has closed short sales knows how to structure offers that have a realistic chance of lender approval, understands the BPO process, and knows what title issues to look for before you are too deep in to walk away cleanly. This is not the transaction to navigate without representation.